You’re sitting in your living room and the number is $14,000, which you can’t write a check for. So the offer becomes “$200 a month, 0% for 12 months,” and suddenly it sounds doable.

Here’s what I’d check before I signed it, because financing windows is fine — if you read which kind it actually is, and whether it comes with a clock.

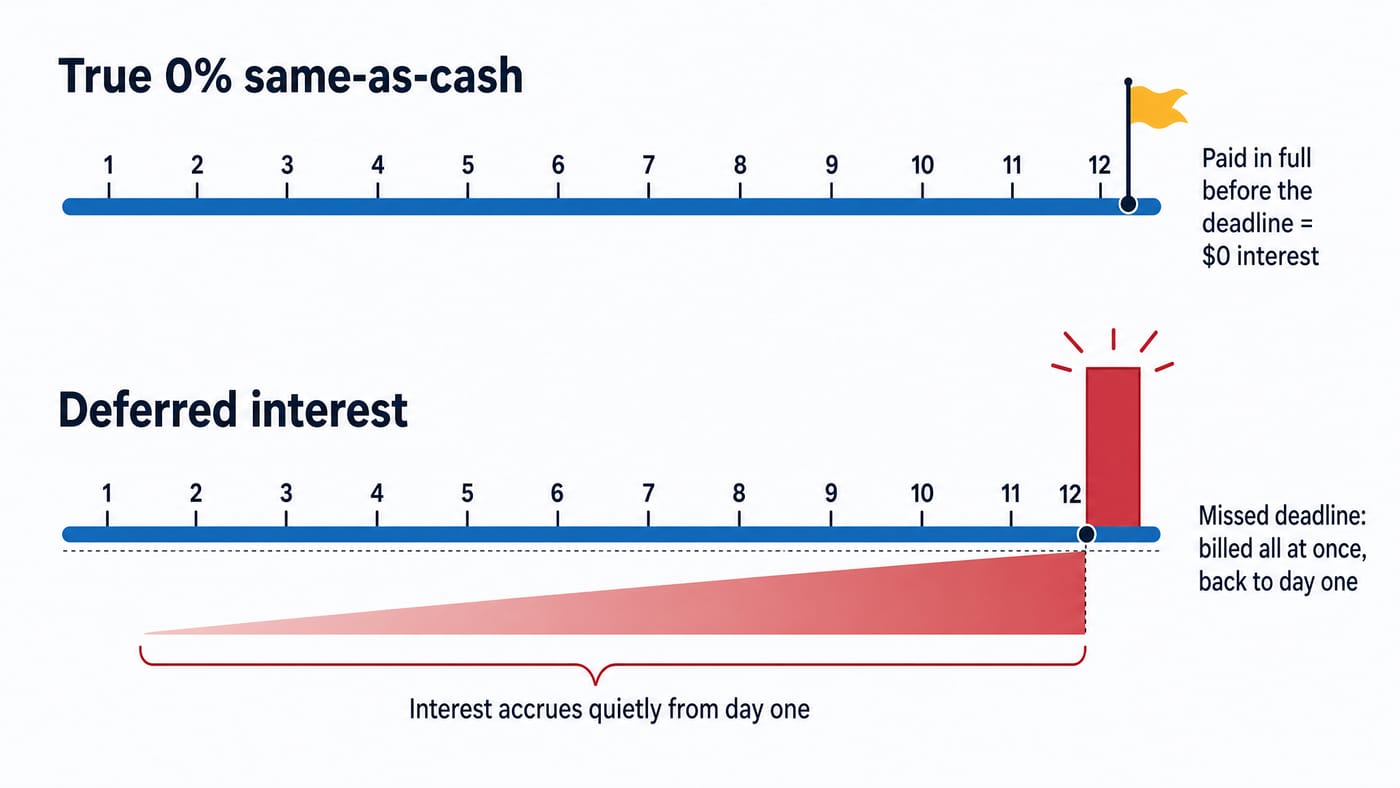

The short version: true 0% same-as-cash that you clear inside the promotional period beats deferred interest, which back-bills all the interest if you’re a day late. And don’t count on the energy savings to cover the payment.

Should I finance my replacement windows? Only if it’s genuine 0% you’ll clear before the promo ends. Watch for deferred interest, don’t bank on utility savings to cover the payment, and compare the company plan against paying cash or a . Decide on the total price, not the monthly number.

The kinds of window financing (and the trap)

There are four common ways to finance, and one of them has a trap built in.

- True 0% same-as-cash — no interest as long as you pay the balance in full before the promotional period ends. This is the good one, if you’ll actually clear it in time.

- Deferred interest — looks identical to same-as-cash on the brochure. The trap: if you don’t pay it off by the deadline, the lender back-bills all the interest that’s been quietly accruing from day one, on the full original principal — not just whatever balance is left.

- Fixed- installment — a set rate over a set term. Honest and predictable, but you pay interest across the whole amortization.

- HELOC / home equity — borrow against your home, often at a lower rate, but it’s secured by the house.

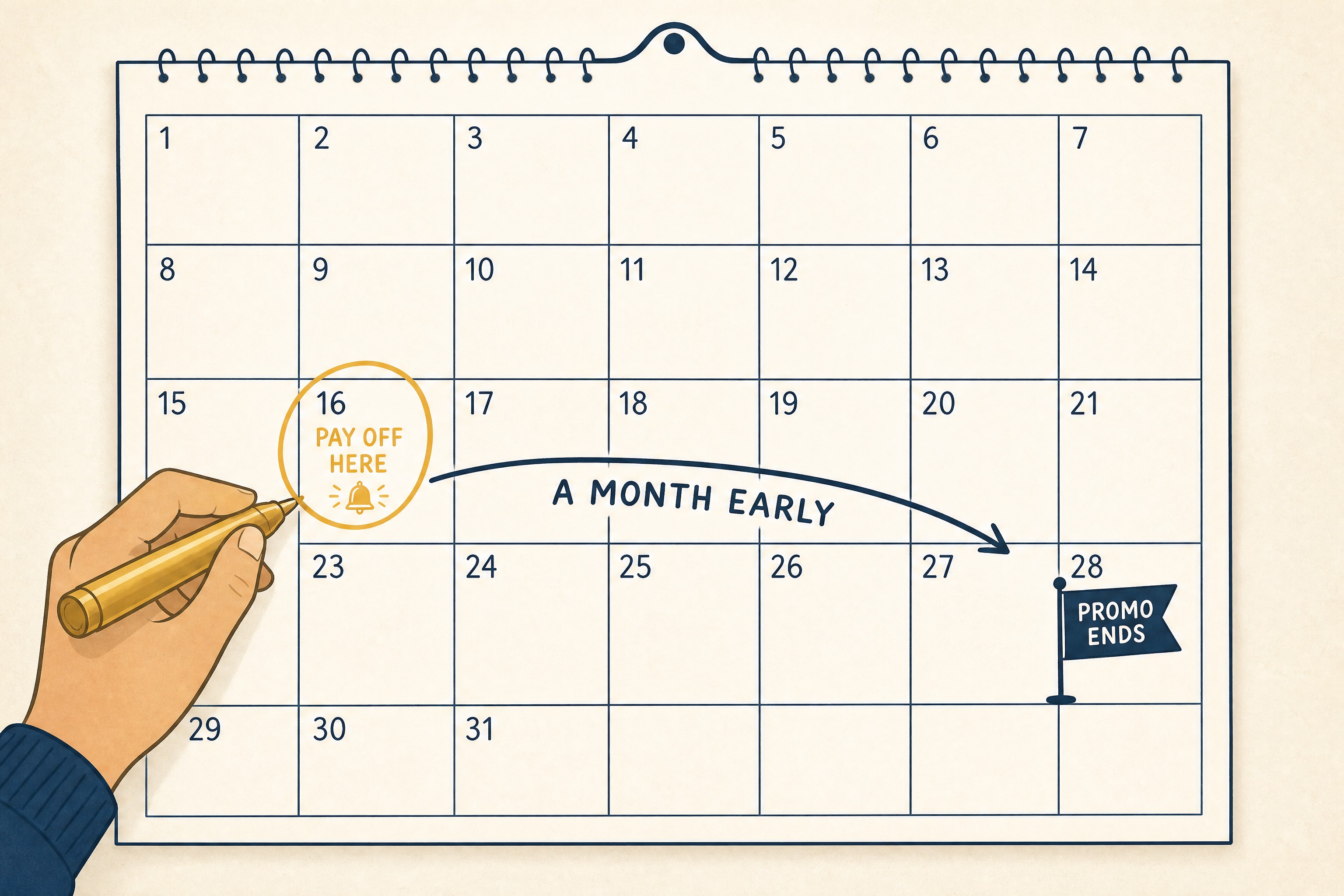

The deferred-interest one is the trap your instinct is right about. Same-as-cash isn’t a gift — it’s a clock. Beat the clock and the money really is free.

Miss it by a day and it flips into some of the most expensive money you’ll ever borrow, because the interest didn’t pause while you were paying — it was accruing the whole time, waiting to be billed.

If an offer hides a catch, this is usually where it’s hiding. So ask the plain question: is this true 0%, or deferred interest?

Will the energy savings cover the payment?

Honestly? Usually not fully. Don’t let “half your payment is utility savings” be the reason you sign.

Efficient windows do trim heating and cooling costs — as a general figure, on the order of 10–15% off the heating-and-cooling slice of the bill, not the whole bill. In a North Carolina climate with a long cooling season, that’s a real but modest number, and it rarely lines up so the savings quietly cover a $200 monthly payment.

When a salesperson nets your payment against projected bill savings, that’s a framing trick, not a budget. I don’t sell windows on payback math here — decide on comfort and the total price, then read why you can’t bank on energy savings to see how modest the number really is.

Company plan vs cash vs HELOC

Each one wins in a different situation. Match the plan to your own math — and always to the total price, not the payment.

| Option | How interest works | Best for | The catch |

|---|---|---|---|

| True 0% same-as-cash | No interest if cleared inside the promo term | You'll pay it off before the deadline and want to keep cash liquid | Becomes a trap if you miss the payoff date |

| Deferred interest | Back-billed in full on the original principal if not cleared in time | Almost no one, knowingly | A single late payoff back-bills all the accrued interest |

| Fixed-APR installment | Set rate over a set term | Predictable payments; you won't clear a 0% in time | You pay interest the whole way |

| HELOC / cash | Lower rate (HELOC) or none (cash) | Lowest total cost, if you have equity or savings | HELOC is secured by your home |

True 0% same-as-cash

- How interest works

- No interest if cleared inside the promo term

- Best for

- You'll pay it off before the deadline and want to keep cash liquid

- The catch

- Becomes a trap if you miss the payoff date

Deferred interest

- How interest works

- Back-billed in full on the original principal if not cleared in time

- Best for

- Almost no one, knowingly

- The catch

- A single late payoff back-bills all the accrued interest

Fixed-APR installment

- How interest works

- Set rate over a set term

- Best for

- Predictable payments; you won't clear a 0% in time

- The catch

- You pay interest the whole way

HELOC / cash

- How interest works

- Lower rate (HELOC) or none (cash)

- Best for

- Lowest total cost, if you have equity or savings

- The catch

- HELOC is secured by your home

Actual rates and promo lengths swing on your credit and the lender, so I won’t quote you an APR that pretends to be universal — get the real terms in writing for your own file.

Run your own numbers

Take the plan you were actually offered and put its numbers in. This is the whole argument of this page in one box: the payment is what you feel; the total is what you pay.

Financing calculator

What does this plan really cost?

Put in the numbers from the plan you were offered. The payment is what you feel monthly — the total is what you actually pay. Compare plans on the total.

Estimates from your inputs using standard amortization — real plans can differ in fees and compounding. No rates are suggested here; get the actual terms in writing.

Whatever you compare, anchor on the total price, not the monthly payment. That’s the whole game: payment-vs-price. Sanity-check the total first — here’s how to sanity-check the total, not the payment — and against what windows actually cost.

Financing red flags

These are the signs the financing is being used to sell you, not serve you.

- Payment-only quotes — they’ll tell you “$200/month” but won’t put the total price on paper. If they won’t write down the cash price, that’s the tell.

- Pressure to sign for the rate — “the 0% is only good today.” A real rate doesn’t expire at midnight, same as a real price doesn’t.

- Deferred interest sold as “0%” — the promo says zero, the fine print says the interest is accruing. Ask which one you’re actually signing.

- Prepayment penalties — you get charged for paying it off early. Ask before you sign, not after.

Cross-check these against the full list of payment-plan red flags.

The four questions to ask before you sign

Copy this and read it out loud to whoever’s holding the pen. If the answers don’t come easily and in writing, that’s your answer.

Ask the salesperson, on paper:

- Is this true 0% same-as-cash or deferred interest?

- What’s the total price — the cash price, not the monthly payment?

- What’s the total financed cost if I make the minimum payment the whole term?

- Is there a prepayment penalty for paying it off early?

What to do next

Get the real number and the honest financing picture in the same conversation — without the payment-plan pressure.

If you want someone to give you the actual total price and walk you through which kind of financing you’re really being offered, that’s what the consult is for.

Book a no-pressure consult and we’ll separate the price from the payment so you can decide with clear math on your own terms — and on your own clock!

Sources, Verification & Fact-Checking verified July 2026

Every load-bearing fact on this page is sourced and verified against a primary authority.

Verified July 2026 via direct review of the cited authority — the links open the controlling source so you can check it yourself rather than take our word.

- Deferred-interest promotions can back-bill interest retroactively on the original balance. With a deferred-interest offer, if you don’t pay the full balance by the end of the promotional period (or you’re more than 60 days late on a minimum payment), the lender charges interest accrued from the original purchase date, not just on the remaining balance — as CFPB puts it, “you would owe all of the interest back to the original date of the charge.” This is the mechanism that separates “deferred interest” from a true 0% offer. (view source — CFPB, “No interest if paid in full — how does this work?”)

- Read the actual financing terms — APR and promotional length depend on your credit and the lender. Specific rates, promo periods, and fees are not universal and are not stated here; confirm them in writing for your own quote. Under the Truth in Lending Act, lenders must disclose the cost of credit — the APR reflects the interest rate plus fees charged when the loan is made. (view source — CFPB, interest rate vs. APR)

- Energy savings from efficient windows are real but modest (~10–15% of heating and cooling costs). Directional general figure, not a payback promise — do not count on utility savings to cover a monthly payment. (windowsresource knowledge base, grounded from general industry energy figures; not a per-home guarantee.)

- HELOC / home-equity borrowing is secured by your home. A home equity line of credit uses your house as collateral, which is why its rate is often lower than an unsecured plan — and why the stakes are higher: as CFPB warns, “if you fall behind or can’t repay the loan on schedule, you could lose your home.” (view source — CFPB, “What is a HELOC?”)